One of the most interesting qualities of cryptocurrency is how there are multiple avenues to make money. Investors seeking to earn substantial profit can do so without engaging in trades. In this article, we discuss cryptocurrency lending, including its history, how it works, the perks of lending your crypto, and a variety of other things you need to know.

History of Cryptocurrency Lending

Cryptocurrency lending originated in 2020, during the early days of the coronavirus. Due to the effects of the pandemic, banks cut interest rates, forcing people to find alternative ways to earn on their money. In response to this, the crypto market emerged with a lending solution. There, investors could take advantage of attractive rates while retaining full ownership of their cryptocurrency.

Today, crypto lending is pretty much the norm. Rather than the timeworn method of HODLing to make a profit, asset owners can put their tokens to work. Borrowers can also expand their portfolio, gaining more from the tokens they collateralized.

How Does Cryptocurrency Lending Work?

A straightforward way of understanding crypto lending is to consider the format of bank loans. There, your bank uses money from your savings account and rewards you with a certain amount of interest. Similarly, cryptocurrency platforms lend your assets to borrowers who pay interest on the loans they take. Part of this interest is returned to you. Lenders can earn as high as 8 to 12% interest on their funds.

In even simpler terms, three parties exist in a crypto lending relationship in CeFi. The first is the lender who has assets they would like to earn on. The second is the borrower who needs funds for an endeavor. While the third is the platform that can link both individuals with each other.

When taking a cryptocurrency loan, remember that they are always overcollateralized. This means that due to the volatile nature of the crypto space, you put up more collateral than the loan you intend to take, usually stored securely in your crypto wallet.

Why Should I Lend My Crypto?

The following are reasons why you should lend your crypto:

- Lending enables you to access high interest rates, something that you do not get in traditional banks

- It shift from the old method of HODLing which may end up not yielding results. With lending, you out your unused coins to work

- Also, you retain ownership of your cryptocurrency. The arrangement allows you to lend it to the platform without losing proprietorship as you would when you sell.

What Are Crypto Lending Use-Cases?

Cryptocurrency lending has several common use-cases: reinvesting, short-selling, diversification, daily purchases, and many more:

- Reinvesting — you can borrow your holdings against stablecoins and spend received funds to stack more of the same currencies you hold. As the market grows, you sell your accumulated assets and payoff the loan while keeping the profits due to price difference (bullish market case);

- Short-selling — you can borrow your stablecoins against chosen assets (for example Bitcoin or Ethereum) and sell received cryptocurrencies at the current exchange rate. As the market drops, you buy the same amount of Bitcoin or Ethereum cheaper to payoff the loan while keeping the profits due to price difference (bearish market case);

- Increase your passive income – take out a crypto loan and add the released funds to earn even more passive income;

- Diversification — you can borrow your holdings against stablecoins and spend received funds to diversify your portfolio and buy more of different currencies;

- Daily purchases — you can borrow your holdings against stablecoins, exchange them for fiat and spend received funds for your regular needs such as rent or travelling;\

- Pay in crypto – release additional funds for different crypto purchases with the help of merchants. Buy food, clothes, services without converting your crypto to fiat;

- Join any Metaverse – you can engage in your favorite Metaverse project by taking out a crypto loan and buying any token supported inside this Metaverse. Just imagine – still hodling your assets and using all perks of crypto Metaverses at the same time.

I Want To Take A Crypto Loan. What Should I Know?

When you wonder how to get a crypto loan, all you have to do is decide on the amount you require and select a secure site. Verify the website’s availability of the tokens you require and that the minimum yearly interest rate is acceptable to you.

Next, decide on the type of loan to collect — whether a collateralized loan will work for you, or you can use a flash loan to get a quick profit on the sale.

Also, there are several crypto lending parameters that should be understood and constantly kept in mind: LTV, APR, loan time frame, liquidation and liquidation price.

- LTV (Loan-to-value) is a ratio of the loan to the ratio of the collateral. In terms of cryptocurrency lending loans are always overcollateralized which means you receive only a part of your collateral value;

- APR (Annual percentage rate) is the interest rate for the whole year applied on a cryptocurrency loan;

- Time frame defines how many time you have to payoff your cryptocurrency loan;

- Liquidation is a process of selling your collateral to cover the lender’s expenses;

- Liquidation price is a price when the collateral is being sold to cover the lender’s expenses. It is determined before taking the loan.

How to Choose the Right Crypto Lending Platform?

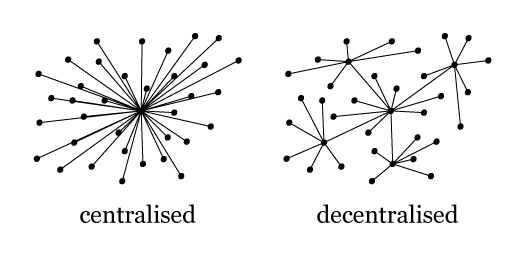

Wondering how to lend crypto, you’ll need to choose a platform that belongs to one or the other type — DeFi vs CeFi.

DeFi is decentralized finance. On such a platform, there will be no intermediaries between the investor and the borrower. The services are based on publicly available blockchain platforms and are completely transparent. You can manage your own money without relying on banks or other financial institutions. However, you’ll have full responsibility for what happens to your assets.

CeFi, centralized finance, offers more guarantees. That said, most platforms will not require you to go through the KYC process. There are strict security measures, so you can be assured of the safety of your asset. Loan is borrowed exactly from the platform itself. The borrowers pay an interest rate to a central supplier, who then transfers the loan right to your wallet.

Other CeFi benefits:

- Risk sharing.

- More flexibility in conversions

- Confidentiality and transparency

Centralized Finance Platforms Compared

| YouHodler | Nexo | Binance | CoinRabbit | |

| KYC process | Yes | Yes | Yes | No |

| APR | 19% – 24% | 18.9% starting point; 10.9% – 18,9% with NEXO tokens | Depends on the token | 17% |

| Loan terms | 12 months | 12 months | 7, 14, 30, 90, and 180 days available | 30 Days/ Unlimited |

| Minimum deposit | $0 | Depends on the token | $0 | $100 |

| Collaterals | 50+ | 50+ | Over 50 | 300+ |

Decentralized Finance Platforms Compared

| Compound | Aave | |

| KYC | No | Yes |

| APR | Algorithm-driven, stablecoins < 4% APR | ETH < 3% APR, USDC > 16% APR |

| Loan terms | Borrowers can end loan at any time | Unlimited |

| Minimum deposit | – | – |

| Currency pairs | ETH, DAI, BTC, USDC, BAT, SAI, REP, WBTC | 12 |

Types of crypto loans

Now, when you understand what crypto lending is, let’s talk about different types of loans that can be most advantageous depending on your original goal.

Collateralized loans

This is one of the most popular types of loans and probably the most convenient. Most platforms require loan collateral, in which the loan-to-value (LTV) ratio usually is set on your choice, as the volatility of the cryptocurrency is high, you can control your own risks with this setting. For example, if the ratio is 50%, meaning that the collateral is twice as much as the loan itself. In the event that the collateral becomes below the value of the loan or a certain set value, it can be liquidated, if you missed the margin call notifications.

The main advantage of secured loans is that often you do not need to provide personal information, which speeds up the process of obtaining a loan.

Flash loans

If you wonder how to borrow against crypto and don’t pay the deposit, there are other options. For example, a flash loan. Such loans are issued and repaid within a single block. That is:

- You take a loan.

- You buy cryptocurrency with it.

- Sell it.

- Repay the loan immediately.

There are risks with this type of loan because the lending process is controlled by a smart contract and does not require human involvement. If you fail to repay the loan in time, the transaction will be canceled.

Uncollateralized loans

As opposed to collateralized loans, uncollateralized loans will require other guarantees. That means you’ll need to fill out an application, submit documents, and undergo a personality and credit check before you’ll be approved.

Is Crypto Lending Safe for Borrowers? What Are the Risks?

It’s normal to have concerns and wonder if cryptocurrency lending is safe if you’ve never taken out a loan before. Although there are a lot of secure platforms available these days, selecting a CeFi platform can give you additional peace of mind if you want more assurances.

The cost of the collateral is a major risk for borrowers. It may result in liquidation and a margin call if its value falls sharply. But, if the market changes, you can always add more collateral. As the primary cause of borrowers losing their assets in crypto lending, it is crucial to keep a close eye on changes in the price of cryptocurrencies, as each collateral has a liquidation price.

The loan-to-value (LTV) ratio is another crucial element. An LTV of 30%, for instance, indicates that your Bitcoin collateral must decrease in value by 30% before it can be sold.

In order to reduce the risks:

1) Make your own investigation. Crypto lending should be thoroughly understood before engaging in, just like any other financial activity.

2) Don’t lend out cryptocurrency that you plan to cash out soon. For crypto lending, long-term or mid-term strategies work best.

3) Avoid using highly unpredictable assets as collateral.

4) Don’t overdo it. Handle cryptocurrency lending with the same caution and responsibility as any other financial activity, and only use funds that you can afford to lose.

CoinRabbit, the Easiest Way to Borrow Crypto

At CoinRabbit we created a comprehensive solution to provide you with the best crypto lending experience.

Easy to Use

The process of lending crypto at CoinRabbit is very simple and easy. Literally, a few clicks to get your funds. You don’t have to browse through the whole website to learn what to do.

Fast and Furious

It takes under 10 minutes to receive your USDT/USDC loan. Forget about waiting for your funds for hours.

No Verification

We do not identify our clients, we do not know where you are from and who you are. We just need your phone number or email. In most cases passing KYC is not needed (required for the cases when the funds can’t pass AML security level).

24/7 Human Support

Use our round-the-clock support to get assistance whenever you need it. Help is only a message away, so there’s no need to wait for business hours.

DISCLAIMER: The information provided in this article is for educational and informational purposes only and should not be construed as financial advice. Cryptocurrency investments carry a high level of risk, and it is essential to conduct thorough research and consult with a qualified financial advisor before making any investment decisions. The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of any financial institution or organization. Always invest responsibly and consider your individual financial situation before making investment choices.

Last Updated on August 15, 2025 by Dan Marsh